Upside momentum continues, but optimism might be way too high

- New stimulus announcement, accelerated vaccinations, improving macroeconomic data and encouraging earnings – all these factors ensured another strong month for global equities;

- Various indicators point that investor optimism levels might be exceedingly high, which may lead to either slower rise or even reversal in equities in May.

April was relatively calm month for global financial assets. Momentum in equities continued to push them higher to new all-time highs, while decline in bonds also somewhat stabilized. There were no major negative surprises during the month, and key factors that have been influencing markets lately remained in positive territory. So, let us go through most important developments:

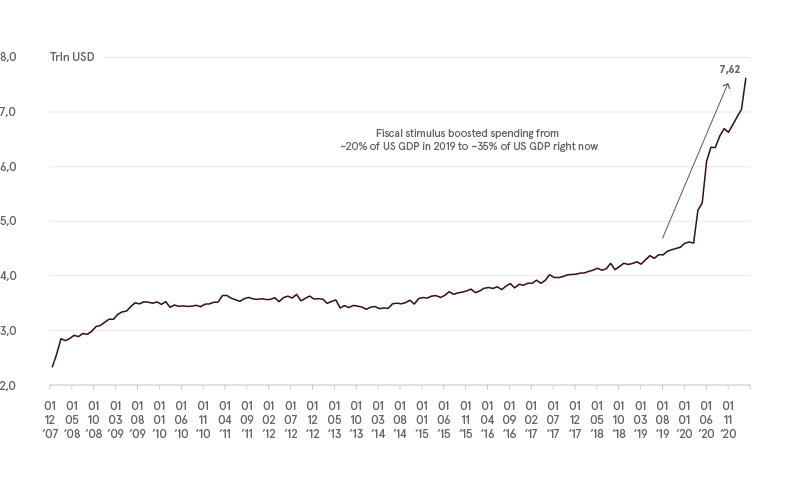

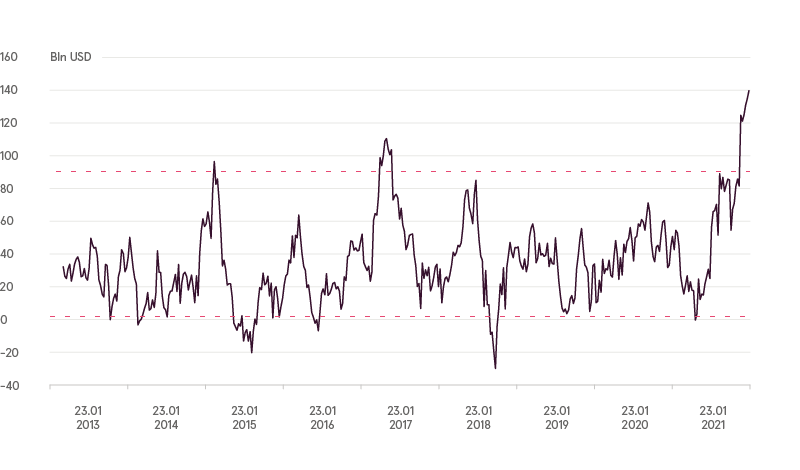

After passing 1.9$ trillion COVID-19 relief package in mid-March and announcing 10-year 2.3$ trillion infrastructure plan in the end of March, Biden administration did not stop and announced yet another government spending plan amounting to 1.8$ trillion also to be spent in next 10 years, but this time to support families. Therefore, since the beginning of the year democrats have already introduced plans for around 6$ trillion in extra stimulus measures, which in relative terms constitutes around 30% of US GDP.

Objectively, new 10-year plans should not be a reason for major investor excitement. Additional government spending would be almost fully financed not by new public debt, but through rising taxes on corporations and wealthy individuals. For example, in April it was also announced that capital gains tax for certain wealthy groups would be almost doubled to around 40% from current 20% in the future.

However, for now investors prefer to ignore these to be felt latter negative consequences and are mainly focused on positive aspects - there would be much more spending. Demand for equities, especially in USA, continues to remain strong and rising.

Trailing 12-month US government spending

Source: Bloomberg Finance L.P.

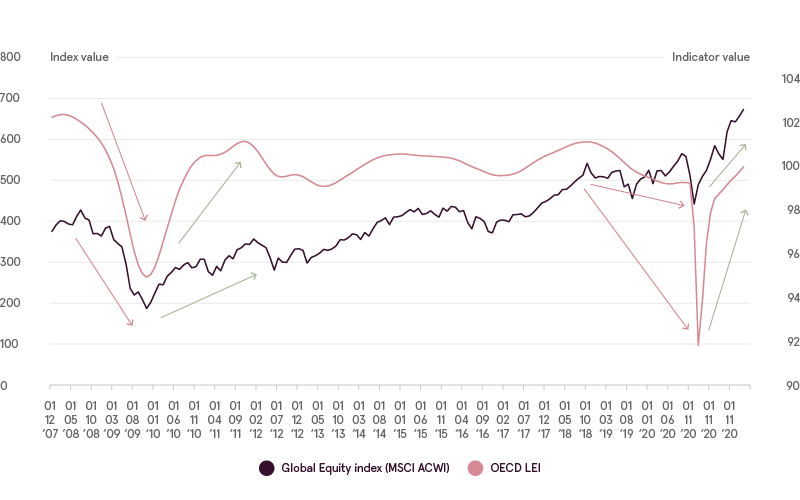

At the same time already implemented fiscal stimulus measures related to COVID-19 and not just in USA continue to ensure that most of population is not losing their pre-COVID ability to spend. As a result, it is being translated to continuously higher consumption of goods since last summer and on balance improving global macroeconomic data as proxied by OECD leading economic indicators index. Until there would be first signs that these improvements are coming to end, it is also unlikely to expect that investors would rush to take profits in their equity positions.

OECD LEI vs global equities

Source: Bloomberg Finance L.P.

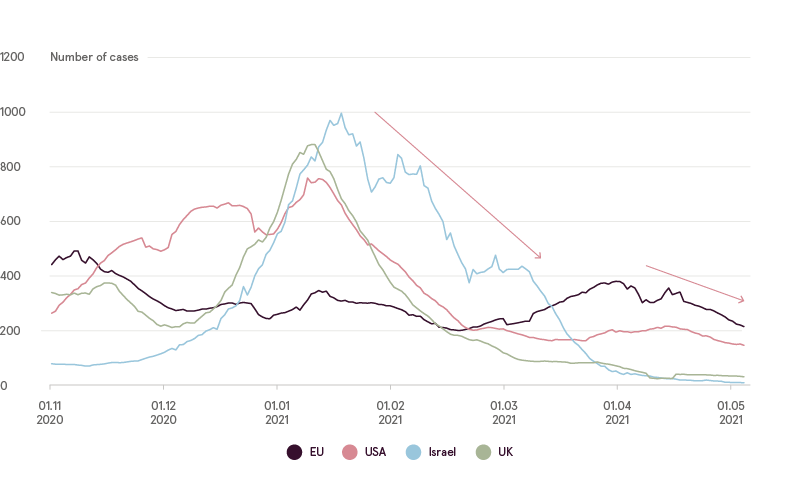

Speaking of COVID-19 trends, here as well data continues to remain encouraging. On the one hand, it is true, that due to drastic situation in India, number of new confirmed global daily cases has set new world record in April. On the other hand, relative to population these numbers are still quite low and remain much better globally than for example in Europe. What is more important, however, that in all countries, where large number of people have already vaccinated, number of new cases is falling at a steady pace. In April, list of such regions was also joined by EU, where vaccination process has finally accelerated compared to previous months.

New daily COVID cases relative to population

In addition, in mid-April companies started to publish their results for first quarter 2021. Based on Refinitiv data, S&P-500 companies are expected to show 46% higher earnings compared to same period last year. Such large growth is not surprising given that global economy became fully paralyzed last March, and majority of companies in essence just stopped working for a while back then. So, what is more important for investor optimism right now, is whether enterprises can even exceed such growth, and show better results than it was estimated. And indeed, out of 303 companies in S&P-500 that have already reported earnings by April 30th, 87% were able to show positive earnings surprises, while usually only around 65% of companies are able to beat analyst estimates on average. In addition, 79% of corporations revised their estimates of future earnings higher. As a result, it also boosted enthusiasm among investors and analysts that corporate results for the remaining 2021 quarters could turn out even better as well, and therefore there is still plenty of room for further upside in prices of indices.

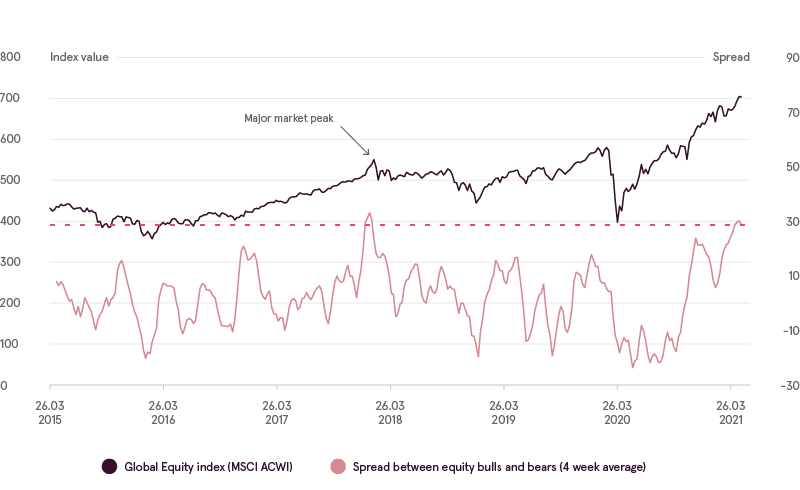

Overall, positive news flow, like what is observed currently, helps to sustain buying interest among investors and keep equity prices rising higher, which we also see happening right now. However, when excitement becomes too stretched and excessive, turning into full-fledged euphoria, this is also the time when becoming a bit more cautious might be helpful. But are investors euphoric right now? Some measures say that they certainly are.

First, let us look at survey numbers provided by American Association of Individual Investors (AAII). Recent data indicates that difference between number of optimists (bulls) and number of pessimists (bears) have reached its highest level in more than three years. To be more precise, last time AAII consensus was so high happened in January 2018, only few weeks before major market top in global indices, which marked start of global economic slow-down and chaotic market behavior in the consequent years.

AAII bull-bear difference vs global equities

Source: Bloomberg Finance L.P.

In addition, high demand for making new investments in equities is also reflected in ETF inflow data. Cumulative ETF purchases over the course of last three months turned out to be record high, significantly outpacing such peaks observed in previous years.

ETF inflows

Source: Bloomberg Finance L.P.

Data on margin debt, i.e. how much money investors borrow to invest in markets also suggests major ongoing excitement. Last two times when growth in margin debt was so high happened in 2000 and 2007, several months before major market peaks.

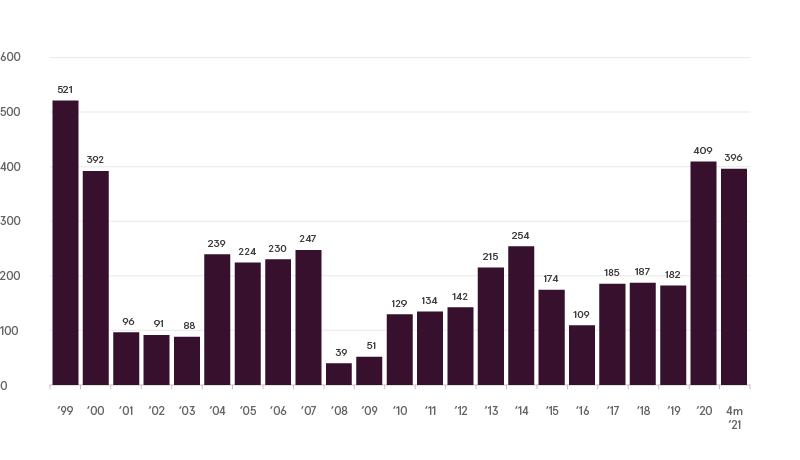

But though above-mentioned indicators are excessive, they still probably do not look as extreme as numbers on investor optimism in relation to initial public offerings (IPO). Here, executives of newly listed companies were able to turn prevalent market excitement totally in their favor. Just in first four months of 2021 number of IPOs in USA reached roughly the same number as during the whole 2020, which in its turn was also record high year since the 90s. Indeed, last time such euphoria towards new stocks was only observed during dot-com bubble, when investors rushed to buy “hot” internet stocks that were expected to become the future, but in the end many disappearing into oblivion.

Hard to say what would happen now, but given that that many of new publicly listed companies start trading at excessively generous valuations and part of entities do not even do IPOs, but appear in the market through being merged to Special Purpose Acquisition Companies (SPACs), where process of financial disclosures and future projections is much less strict, it would not be surprising to us, if many of investors in newly issued enterprises would get burnt in the end similar to how it happened after burst of “dot-com” bubble.

Number of new IPOs

Source: Bloomberg Finance L.P.

Excessive optimism usually means that majority of market participants have already invested and there is not much free cash left on the sidelines. Demand gradually starts to dry up, while those who were able to invest early on start taking profits. As a result, markets reverse and go lower. Will excessive optimism prevent markets from going higher in May? Not necessarily. But given that in four months equities have already increased by more than 10% in EUR terms, we should not be surprised, if rate of change to new highs would become at least slower. Otherwise, May looks as promising as April, and path of least resistance still remains up.

Warnings

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from the Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, represented within the Republic of Latvia by Luminor Bank AS Latvian branch, reg. No 40203154352, address: Skanstes iela 12, LV-1013, Riga, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Latvian Financial Supervisory Authority (Finanšu un kapitāla tirgus komisija). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Latvia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question, and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument, a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to internal rules on sound ethical conduct, management of inside information, handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.