Evidence of rising inflation and its repercussions for financial markets

- Equities and bonds went sideways in May as positive factors were neutralized by excessive sentiment and risk of rising inflation;

- There is still more room for upside in equities, but divergencies between equity sub-segments are likely to persist;

- During the month we increased equity exposure through additional investments in funds that offer inflation protection.

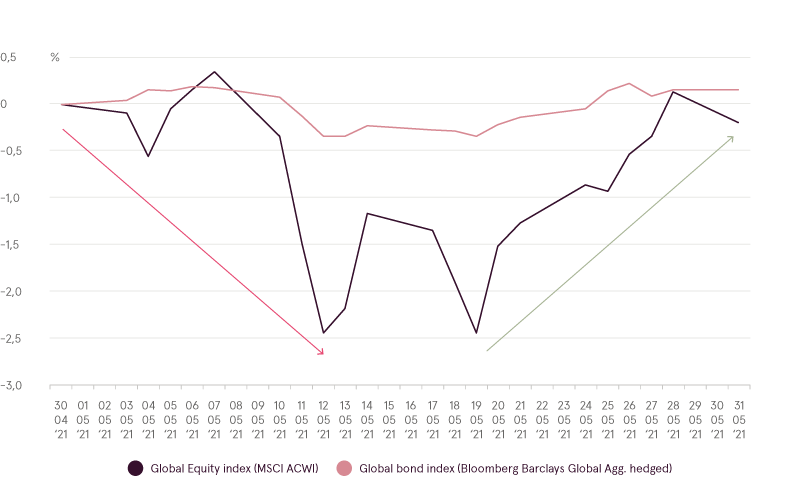

In early May we outlined that though there are plenty of factors to boost equity prices to even higher levels, excessive optimism indicates that markets may be ripe for reversal. During the month indeed we saw both price reversal and consequent recovery, with majority of equity indices closing flat for May. But key reason for sell-off was not related only to sentiment, investors became increasingly worried about rising inflation as well. On the bright side, positive developments, such as steady reduction in COVID-19 cases, new fiscal announcements, rising earnings and improving macroeconomic data still prevailed, and by the end of the month majority of equity indices were able to return close to their all-time high levels.

Equity performance in May

Source: Bloomberg Finance L.P.

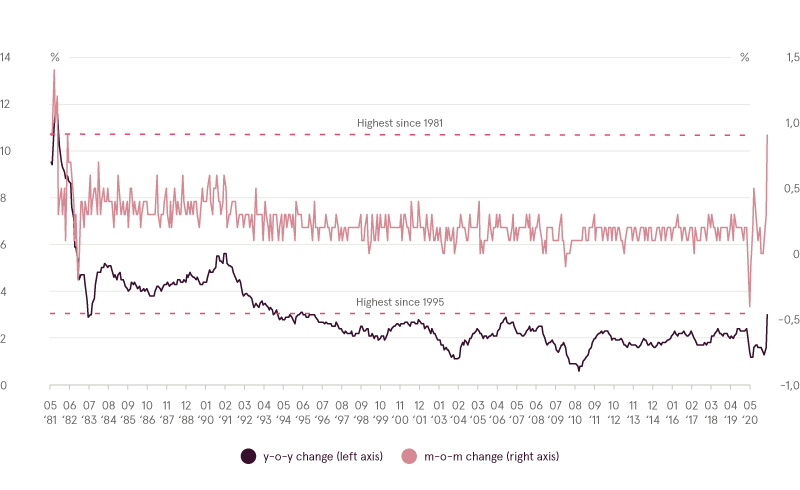

Topic of inflation remains hot since the beginning of the year and in May its importance has only intensified. Latest data on core consumer price index (core CPI)1 from USA shows that monthly change in prices of 0.9% in April was the highest since September 1981 (almost 40 years). Meanwhile, annual change in core prices in USA has reached 3%, highest value since 1995. Given that since last October each new monthly release shows only signs of price change acceleration, not surprising that more and more investors start to believe that inflation may soon become uncontrollable, and especially so, if US government and Central bank would continue to pursue very loose fiscal and monetary policies.

US core CPI (monthly and annual)

Source: Bloomberg Finance L.P.

On the other hand, FED so far believes that high inflation is only transitory, and it will not be sustained for long after full economic reopening. It is true, that due to COVID-19 restrictions suppliers right now are not able to fully cover all consumer needs, with excess demand putting pressure on prices. However, when all business operations would be restored and companies would also be able to expand their production facilities, price stability is likely to be regained as well. There would be no overheating any more. Such scenario is quite reasonable and definitely could happen. Problem is that it is not a guaranteed outcome, and if the FED ultimately is wrong and inflation would continue to spiral out of control, investors may become severely punished from incorrect positioning in certain assets. Nobody wants to take such risk and therefore in 2021 we are seeing rather significant outperformance of financial assets that benefit from inflation and underperformance of securities that are unable to protect from rising prices.

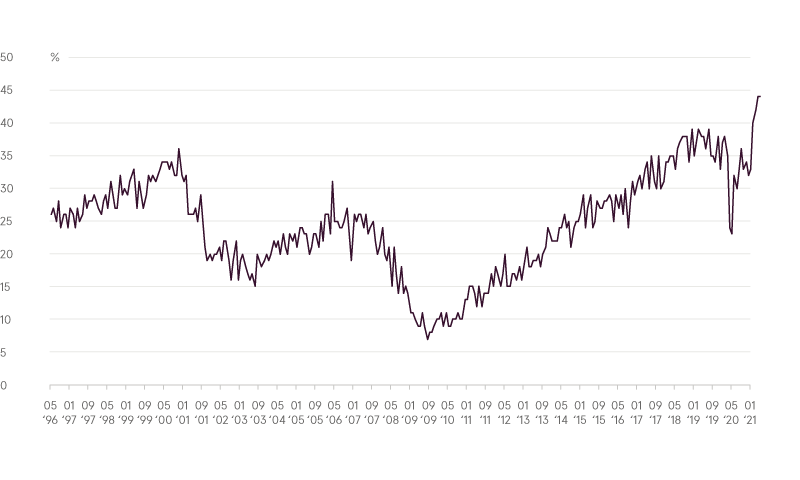

But why, contrary to FED’s opinion, high inflation might turn out to be permanent? Different factors may be in play. For example, to increase supply producers would still need to hire additional skilled labor, and recent NFIB2 data shows that employers have severe difficulties in finding such employees. Record high 44% of small businesses said that they have open vacancies, unable to fill, as there are no suitable applicants for the job. And this is despite number of unemployed in USA still being by 4 million higher than in early 2020 before COVID-19. Potential solution to this problem is obviously to increase proposed wages, and make job offers more attractive. But the likely outcome of this development is also to pass wage increase to consumers, so that companies are not losing their profits. In essence, that is how cost inflation persists.

Job openings hard to fill

Source: Bloomberg Finance L.P.

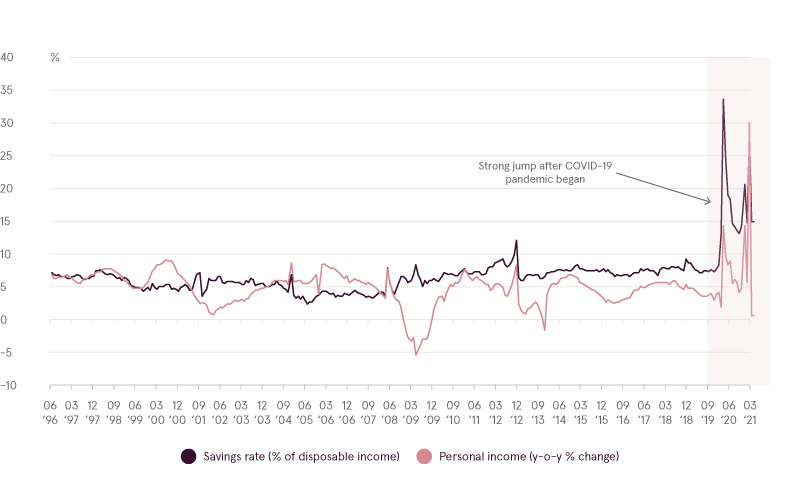

Another option to create persistent inflation is through rising demand. During pandemic, savings rate of population has jumped considerably compared to last 50 years. Through fiscal measures, majority of population also did not experience decline in their personal income throughout last year. In addition, to support economy FED has increased money supply at the highest rate since World War 2. Now, after reopening, there is risk that all this saved and newly created money would start to pour into economy, significantly increasing consumption from current levels. As too much money would be having too few goods to chase, with suppliers unable to produce adequate amount of inventory in a timely manner, inflation might be able to persist once again.

Savings rate and personal income

Source: Bloomberg Finance L.P.

Unfortunately, nobody knows for sure which exact scenario would play out, but given actual data, odds are shifting more and more towards persistently higher inflation. As a result, expectations that central banks would have to introduce tighter monetary measures earlier than planned also increase. Possibility of higher interest rates puts downward pressure on longer term bond prices and causes investors to reallocate to specific “inflation protection” segments in equities.

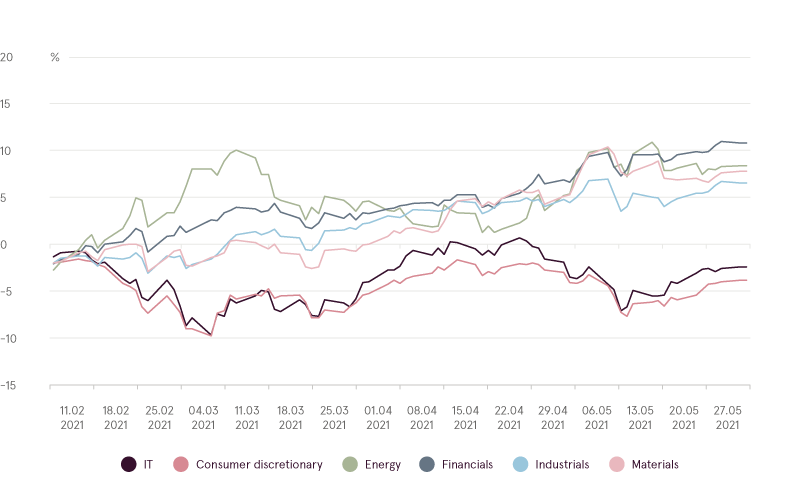

This development is vividly seen since mid-February, as best 2020 sectors such as IT and consumer discretionary are struggling to show positive performance, while sectors such as materials, financials, energy and industrials that tend to profit from inflation continue to show strong uptrend.

Performance of various sectors YTD

Source: Bloomberg Finance L.P.

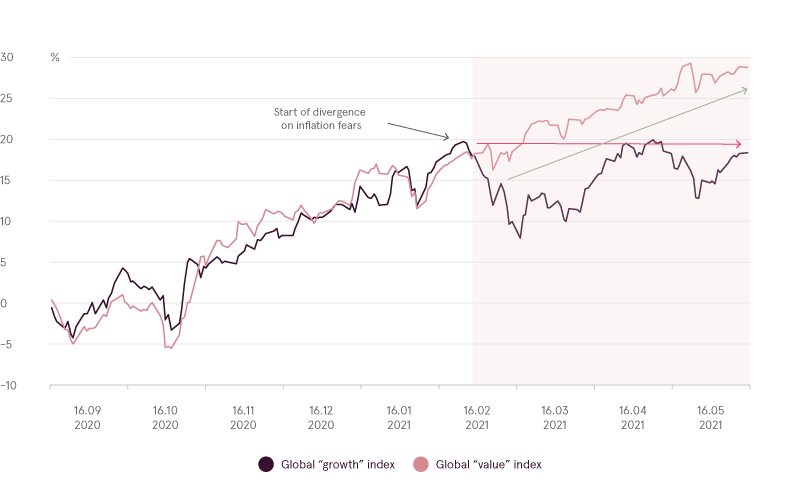

Same phenomenon is observed also when market is analyzed through “growth” vs “value” perspective. In normal conditions equities of companies with strong earnings growth and equities of cheaper cyclical, often more mature corporations tend to move in unison, though rate of change may be different. However, since mid-February we see massive divergence between two equity investment style universes. Prices of growth stocks are still struggling to exceed levels shown 3.5 months ago, while value stocks during the same time increased by more than 10%.

Performance of growth vs value

Source: Bloomberg Finance L.P.

In client portfolios we continue to hold concentrated equity positions in funds with exposure to “value”, materials and industrials, all of which positions were opened in late January just before divergences have begun. Later in April we also increased weight of financials, followed by increasing weight of energy in May. In addition, we still have reduced exposure in bond universe. As a result, if inflation is to stay and accelerate further, portfolios are positioned to benefit from such outcome.

Unless, some unexpected negative surprises would reemerge in June, there is high likelihood that the markets would continue trending higher this month. There is still enough of positive news impacting financial markets, such as gradual removal of lockdown restrictions happening in multiple countries, rise in global economic activity, improving corporate earnings forecasts and potential plans to have elevated fiscal budgets even after COVID-19 is gone3. Potential turbulence may be caused, if inflation release for May would turn out to be even higher than for April, and FED in mid-June during their meeting would have to somehow address rising investor concerns.

Portfolio Management update

During May we made multiple changes to be better positioned for scenarios of persistently higher inflation and economic cycle rebound. We entered new position in Energy sector and increased weight in UK, which also has higher exposure to commodity producers. Inside emerging markets, we continued to reduce weight of emerging Asia, as Chinese authorities undertake much more stringent fiscal and monetary policies than in the West, and region also suffers from higher exposure to growth ideas in IT and consumer sector. At the same time, we increased weight of Latin America and Emerging EMEA, both regions are exporters of resources and tend to benefit considerably from inflationary pressures. In addition, we sold momentum ETF as it had elevated exposure to underperforming sectors. While undertaking all these changes we also increased total equity weight in portfolios, and reduced cash holdings to minimum. In inflationary environment cash tends to lose in purchasing power, and in May there were attractive opportunities to put this extra cash to use.

1 Core consumer price index excludes changes in food and energy prices, as both have tendency to be highly volatile and distort underlying data.

2 National Federation of Independent Business -largest small business association in USA

3 For more detailed discussion of these factors please see our “May 2021” market update.

Warnings

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from the Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, represented within the Republic of Latvia by Luminor Bank AS Latvian branch, reg. No 40203154352, address: Skanstes iela 12, LV-1013, Riga, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Latvian Financial Supervisory Authority (Finanšu un kapitāla tirgus komisija). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Latvia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question, and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument, a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to internal rules on sound ethical conduct, management of inside information, handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.