Interest rates | Luminor

Interest rates

The new housing variable interest rate loans can be granted by applying a variable interest rate that consists of a 3, 6, or 12‑month Euribor rate + individual interest margin.

The fixed part of the rate is calculated on an individual basis and is set taking into account the customer‘s credit history, the purpose of a credit, the extent of cooperation with the bank, the liquidity of a real estate pledged, etc.

Find out EURIBOR rates

Euribor is a Euro Interbank Offered Rate at which eurozone banks offer to lend funds in euros to other eurozone banks. Euribor is applied on the second business day after its fixing date. EURIBOR is published by the European Money Markets Institute (EMMI).

If the Euribor value is negative, it is equaled to zero.

The Euribor interest rate can change (increase or decrease) depending on the market situation.

The European Union Benchmark Regulation (hereinafter BMR) sets out criteria for reference rates that can be used in financial contracts going forward. Since LIBOR reference rates no longer comply with the mentioned criteria, starting from January 2022, all non‑USD LIBOR settings will cease to exist and will be replaced with reference rates complying with requirements established in BMR.

Luminor has taken into consideration consultations and recommendations from the regulators and external working groups (brought out in Table 1 below) to ensure that the reference rates used for the replacement of the ceased ones are compatible with the market practice and comparable to the existing reference rates.

Table 1. Overview of currently used interbank offered reference rates: replacement rates and timeline

|

Currency |

Libor reference rate |

Status in existing contracts |

Replacement rate |

Dedicated transition working group |

|---|---|---|---|---|

|

EUR |

LIBOR EUR |

Expired on 2021‑12‑31 |

Working Group on Euro Risk‑Free Rates |

|

|

CHF |

LIBOR CHF |

Expired on 2021‑12‑31 |

The National Working Group on Swiss Franc Reference Rates (NWG) |

|

|

USD |

LIBOR USD |

Expired on 2023‑06‑30 |

Due to the fundamental differences between LIBOR and new reference rates (as stipulated in the section above) – to make sure that all market participants are treated fairly and were not discriminated – price adjustments need to be added to the new reference rates that are used in contracts which were originally referencing LIBOR.

The necessity to add a fixed price adjustment to the new replacement reference rates SARON, SOFR, SONIA and €STR is further explained by International Swaps and Derivatives Association (ISDA). In July 2019 ISDA announced that Bloomberg Index Services Limited (Bloomberg) was selected as the vendor to calculate and publish this spread adjustment. Bloomberg has defined the spread adjustment calculation methodology in their “IBOR Fallback Rate Adjustments Rule Book” and published the official fixed values that should be added to the new reference rates when creating a replacement rate. Dedicated working groups (brought out in Table 1 above) have further confirmed through their consultations that adding the ISDA spread adjustment to the new reference rates (SARON, SOFR, SONIA, €STR) is the most appropriate solution. For clarity, the ISDA spread adjustments that are relevant in Luminor’s client credit agreements are brought out below in Table 2 as well.

Table 2. ISDA spread adjustments that need to be added to the new reference rates1.

|

Old reference rate |

O/N |

S/N |

1w |

1M |

2M |

3M |

6M |

12M |

|---|---|---|---|---|---|---|---|---|

|

USD LIBOR |

0,00644 % |

N/A |

0,03839 % |

0,11448 % |

0,18456 % |

0,26161 % |

0,42826 % |

0,71513 % |

|

CHF LIBOR |

N/A |

‑0,0551 % |

‑0,0705 % |

‑0,0571 % |

‑0,0231 % |

0,0031 % |

0,0741 % |

0,2048 % |

1 The ISDA spread adjustment values are not calculated by Luminor. They are produced by a third‑party vendor Bloomberg Index Services Limited to facilitate fair pricing of LIBOR replacement rates. (https://assets.bbhub.io/professional/sites/10/IBOR-Fallbacks-LIBOR-Cessation_Announcement_20210305.pdf)

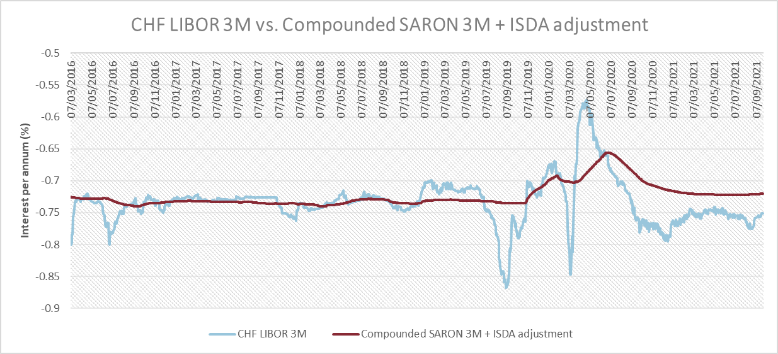

For example, if a 3‑month LIBOR CHF was applied under the current credit agreement, it will be replaced by SARON by adding 0.0031% ISDA (see Table 2) to make the price as close as possible to the base rate of the variable interest previously applied.

Visual comparison of CHF LIBOR and the new Compounded SARON + ISDA adjustment reference rates

Source: Fixed ISDA spread adjustment values published by Bloomberg Index Services Limited

Regulatory bodies

Euribor and the Floating Funding Margin (EBFMI)) annual interest rate consists of Euribor and the Floating Funding Margin (FMI). The interest period of the Base rate is 3, 6 or 12 months. It is calculated by adding a long-term financing margin (FMI) to the Euribor rate that reflects a short‑term borrowing rate. EBFMI may vary depending on the situation in the market, i.e., changes in the FMI and Euribor; thus, it can decrease or increase.

European banks funding rate (EBFMI)

NOTE! New loans are not issued with this interest base.

Euribor is determined, administered, and published by the European Money Markets Institute (EMMI). More information about Euribor.

Floating funding margin – ICE Custom Index Q973. The index reflects the funding spread above Euribor paid by European banks with high credit ratings for long-term funding in Euro.

The index is calculated by ICE Data Indeces, LLC by virtue of bonds’ trades made by European banks with high credit ratings.

ICE Custom Index Q973 is calculated from daily index as the moving average over a 6-month period.

Daily index is calculated based on EUR bonds of European banks with high credit ratings (Composite A- to AA-) in compliance with the criteria as follows:

- Eurozone countries with Moody’s rating of A1 or better, plus Sweden, Norway, Denmark, Switzerland

- Every bank is represented by a single bonds’ issue

- The bonds’ redemption period varies between 4-10 years

- The minimum amount of a single issue is EUR 500 mil.

The Bank applies the value of ICE Custom Index Q973 that has been imposed two business days earlier. More information including information about historical ICE Custom Index Q973 values is available on ICE Index Platform:

1. A new user should register for the limited access:

2. The respective index and the date should be selected on the Home page. For historical data overview the Show Chart option needs to be selected.