Despite all turbulences in the political environment, markets rallied

- European political and energy disturbances

- Finally, ECB made the move

The July was very favorable for developed equity markets. The US S&P 500 index (S&P 500 Total Return EUR Index), which represents major 500 US companies increased by 12.28% during the month. Similar result was delivered by broad developed markets (MSCI World Total Return EUR Index), which generated double digit positive return and increased by 10.67%. Except for Emerging markets where the result was not as good as in developed markets, but also, generated positive 2.28% return. One of the factors which contributed to outperformance of developed markets were better than expected earnings.

The weaker consumer spending and declines in investment both business and residential influenced the contraction in the US economy. US GDP fell an annualized 0.9% in the second quarter after the contraction of 1.6% in the first three months of the year. While the largest economy in the world shrank for a second straight quarter – meeting one of the rules of thumb for defining a recession, economists and Federal Reserve Chair Jerome Powell are still skeptical that US economy will plunge to deeper recession because of the strong labor market. Based on the available data and broad activity it is not yet consistent with a contraction of the economy that is typically thought of as recession. The economists agree that more likely we could face the recession not earlier than at the beginning of 2023. however, the GDP data shows that the economy is slowing down now. The household finances are in good shape right now, so even if the economy goes into recession, they are entering the recession with less leverage and in far better financial condition than they did in previous crises.

Despite that economy may be nearing the recessionary period, Fed policy makers raised their benchmark interest rate by another 75 basis points as they try to bring inflation down to the desired levels in the medium term. The essential fuel for the economy is one of the strongest ever labor markets which allows to have tight monetary policy and fight against elevated inflation.

While US is focused on controlling the inflation, it seems that Europe faces more challenges than elevated inflation and increased energy prices. Current political turbulence in Italy was triggered by one of the governing coalition party boycotts, with prime minister Mario Draghi offering his resignation, which was rejected by the president at the time. Italian President Sergio Mattarella rejected Mario Draghi’s offer to resign as prime minister in a bid to avert a political crisis that would unsettle financial markets and potentially lead to elections in the fall. After unsuccessful attempts to unite the governing coalition, the prime minister Mario Draghi stepped down.

UK prime minister Boris Johnson announced at the beginning of July that he is stepping down form his position. He was forced to do by rebellion of his own cabinet and parliamentary group after three years of continuing scandals.

Unrest did not bypass Germany either. The Russian gas giant Gazprom closed its main pipeline to Europe which ends in Germany. Gazprom declared force majeure event on several European natural-gas buyers signaling that it intends to keep supplies capped. The company has been delivering less gas than ordered by customers over the past month, citing problems with turbines at its main pipeline. Despite that, gas shipments were restored but only at 40% of capacity which was further reduced to only 20% in the end of July. The control of gas supply became the tool of political blackmail.

Regardless the fact that European politics faces unexpected issues and increased uncertainty during this time, the European Central Bank raised key interest rate by 50 basis points, the first increase in 11 years and the biggest since 2000 as it confronts surging inflation. Also, policy makers unveiled a new monetary policy tool which they expect will ensure that markets do not push up borrowing costs too much in vulnerable economies, as happened in 2012.

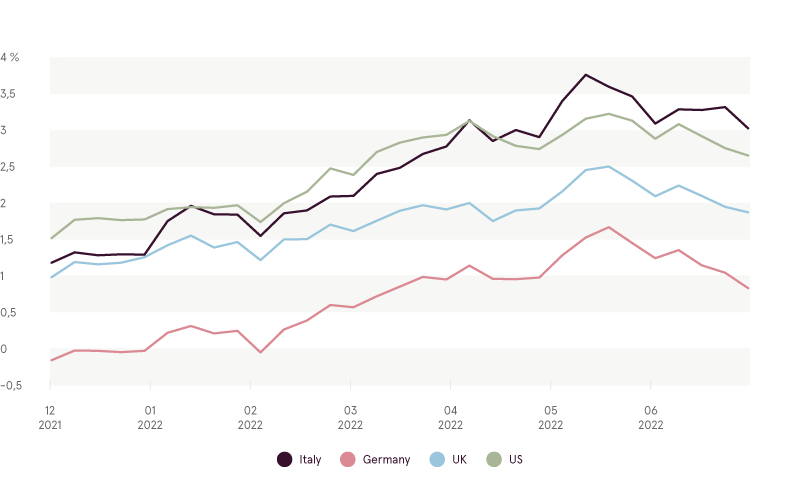

10 year Government Bond Yield

Source: Bloomberg L.P.

Irrespective of all political shocks, bond markets showed resilience. Chart 1 above shows that bond yields decreased (bond price increased) in major regions welcoming central banks’ actions to fight against elevated inflation.

“House view” update

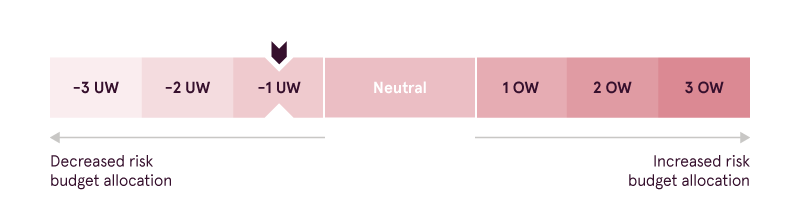

Luminor Investment management team decided to maintain lowered risk allocation budget and higher exposure to defensive sectors (utilities, healthcare, and energy). High uncertainty about possible consequences of the war in Ukraine, tightening monetary policy, high volatility in the markets and slowed economic growth warrant such decision.

Warnings

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from the Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, represented within the Republic of Latvia by Luminor Bank AS Latvian branch, reg. No 40203154352, address: Skanstes iela 12, LV-1013, Riga, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Latvian Financial Supervisory Authority (Finanšu un kapitāla tirgus komisija). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Latvia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question, and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument, a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to internal rules on sound ethical conduct, management of inside information, handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.