New Month, New Highs

- The US equity market reached a new all-time high, while others showed mixed results

- Emerging markets continue to struggle due to negative investor sentiment

- The shape of the US yield curve continues to raise investor concerns, but now is not the time to worry

- Despite high volatility, allocation to emerging market equities improves the portfolio risk adjusted return

- Strong global earnings growth is expected to continue, as analysts improve estimates

- Equities still pay a healthy risk premium and are thus more attractive than bonds

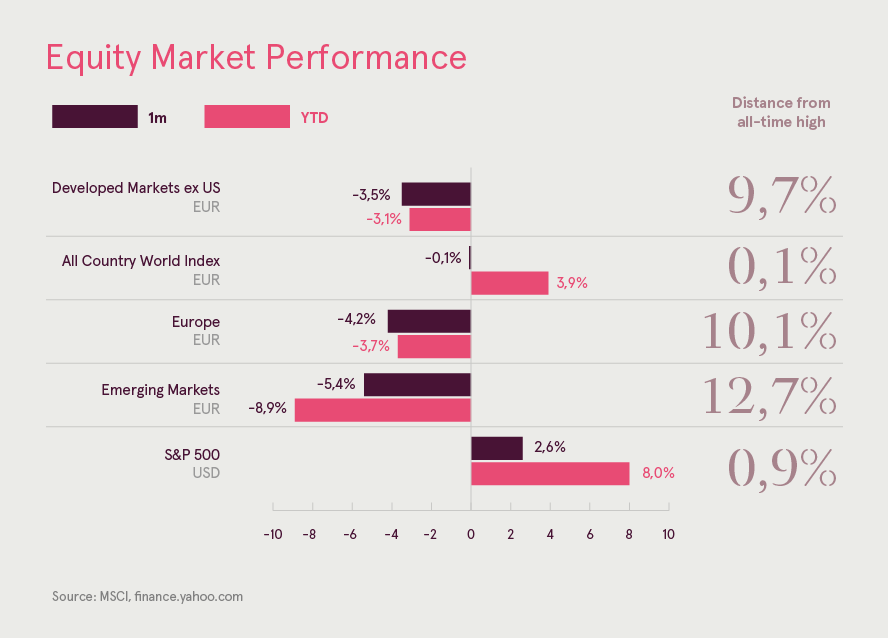

The US equity market reached a new all-time high, while others showed mixed results

Global financial markets finished last month with mixed results. The US equity market has once again taken the lead, buoyed by strong economy and exceptional earnings growth. Confirmation from the Fed President Powell that the economic conditions support the expected gradual pace of rate hikes became the catalyst that propelled the market to new all-time high levels. At the beginning of September, the S&P 500 index was up 8% for the year and within 1% of its record level.

Hampered by political issues and slower earnings growth European equities continued to lag. The European equity index is down 3.7% for the year and around 10% below its record level. Currently negative investor sentiment, however, looks to be stretched. Moreover, indicators show that the economic growth is still stabilised at an above trend level. Political issues, however, are not expected to disappear, impairing sentiment and creating volatility.

Emerging markets continue to struggle due to negative investor sentiment

Sentiment towards emerging markets is still hampered by trade war issues and the appreciating US dollar. As a result, the weakest emerging economies experienced currency crises, where Argentina and Turkey saw massive currency depreciations. Although the problems and their effects were local and contained, the whole emerging market equity index continued underperforming. Emerging market equities were down close to 9% for the year, measured in EUR.

A brief bout of risk-off sentiment in the aftermath of Turkey’s currency depreciation pushed the USD to the highest level in 13 months against the euro. However, the currency pair quickly returned to its latest trading range of 1.15-1.18. Going forward, the path of least resistance looks to be for the euro upside, as the currency is undervalued, economic growth is fairly strong and the ECB should start monetary policy normalisation soon. Consequently, such USD depreciation should reduce the headwind for emerging market currencies.

The shape of the US yield curve continues to raise investor concerns, but now is not the time to worry

August did not bring any major changes in the fixed income space. Benign inflation readings led to a slight decrease in EU and US yields. Flattening of the US yield curve continues to grab investor attention. However, analysis shows that neither the trend nor the current levels of the yield curve are reasons to worry.

Despite high volatility, allocation to emerging market equities improves the portfolio risk adjusted return

The relatively poor performance and high volatility of emerging market equities since the end of the last financial crisis made many question the reasonability of investing in emerging market equities.

The performance difference was even worse if we look at the last year, when emerging market equities declined 4% at the same time as the All Country World index rose over 10%. Price fluctuations are also higher in emerging market equities and historically emerging market equities experience a bear market about once every two years on average.

Analysing longer term performance, however, there is evidence that higher risk is also offset by higher return. Since 1988, emerging market equities delivered an average annual return of 8% compared to 5.6% for developed market equities. Moreover, these two regions do not always move together, which further improves the diversification benefits.

Consequently, adding emerging market equities to the portfolio improves the both the absolute and risk adjusted return (return per each unit of risk). Allocating 20% of the portfolio to emerging markets improves the return by almost 1 percentage point compared to the developed markets portfolio. Moreover, as the increase in risk is very small, the return per each unit of risk grows over 10%.

Strong global earnings growth is expected to continue, as analysts improve estimates

Recent exceptionally strong earnings growth has eased worries about the equity valuation, as growing earnings make equities cheaper. Moreover, global earnings growth is expected to continue at a double-digit pace at least for the next year.

As the tax cut effects wane, earnings growth in the US will moderate. But analysts are still expecting over 13.6% in earnings growth for the year ahead. European earnings are also improving and should grow around 9% during the next year. As emerging market earnings are also expected to grow at 13%, overall global corporate earnings growth should exceed 10%.

Confirming the positive developments in corporate earnings is the number of positive earnings revisions by analysts. Globally, over 72% of expected earnings revisions were positive during the last 3 months. A clear trend of improvement is visible in Europe, where over 78% of earnings revisions were to the upside.

Equities still pay a healthy risk premium and are thus more attractive than bonds

As equities are riskier than bonds, investors demand a premium (additional return) for holding them to compensate for the additional risk. The higher the premium, the more attractive equities are compared to bonds. The risk premium is usually measured as the difference between equity earnings yield and the yield of 10-year government bond.

As US equities currently have the highest valuation, we evaluated their relative attractiveness compared to bonds. US equities currently have a 1.37% risk premium over bonds. Although the premium has gone down since its highs, it is still much higher than the average of 0.14% (since 1962). Therefore, equities continue to be clearly more attractive than bonds.

Outlook

Our outlook remains cautiously positive, as all the main driving factors support equities. Global economic growth, although moderating, is still strong, earnings are growing and global monetary policy remains accommodative.

Still, we also have to acknowledge the risks – potential trade war escalation and its economic effects and political turmoil in Europe. Although the realisation of those risks has a low probability, investors have to be prepared for higher volatility.

Warnings

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from the Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, represented within the Republic of Latvia by Luminor Bank AS Latvian branch, reg. No 40203154352, address: Skanstes iela 12, LV-1013, Riga, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Latvian Financial Supervisory Authority (Finanšu un kapitāla tirgus komisija). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Latvia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question, and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument, a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to internal rules on sound ethical conduct, management of inside information, handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.