French toast for Christmas

- French government collapses, yields shoot higher

- South Korean war that never was confuses the markets

- European Central Bank (ECB) keeps the pace with an interest rate cut

- The Federal Reserve (FED) startles the markets

The first half of December has turned out to be a yet another seasonally strong period for the financial markets that brought plenty of festive vibes for investment portfolios of wide range. No matter the political drama or occasional macroeconomic data disappointments, markets have largely continued low volatility optimistic trading, inspired by reignited strength in the market-leading sectors. However, with only few days left until Christmas, FED has announced their plans to slow down the pace of interest rate reductions next year, sending the financial markets into the tailspin.

As a result, developed markets’ equities (measured by MSCI World index in EUR) have tanked by 0.74%, while emerging markets’ equities (measured by MSCI Emerging Market index in EUR) have risen by 1.86%. During the same period yields on bonds were climbing, with 10-year U.S. Treasury bond yields rising to 4.57% from 4.18% a month ago, while German 10-year Treasury bond yields have risen to 2.37% from 2.08% a month ago.

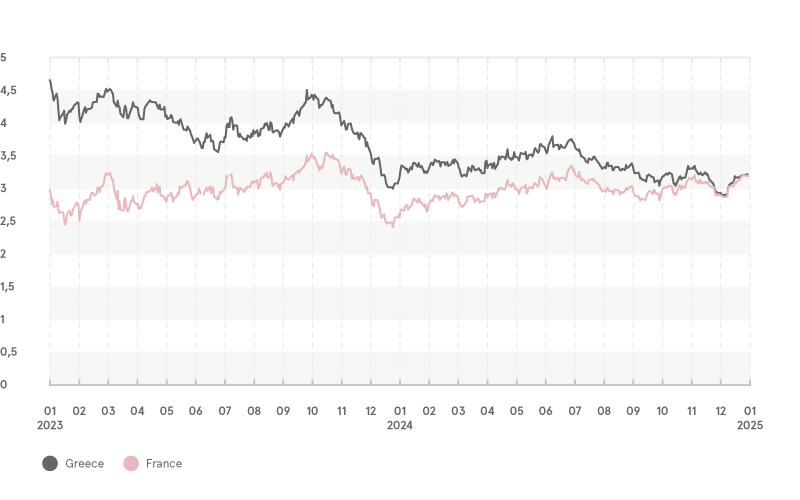

French government collapses, bond yields surpass Greece

The election gamble that French president Emmanuel Macron has placed just before the summer Olympics seems to have been in the focus for several months in a row. Even though the president has picked a moderate Michel Barnier (former Brexit negotiator on the EU side) to lead the minority government, the political deadlock has appeared too challenging even for such an experienced politician to navigate. As there seems to be lack of political will to limit spending in the French parliament post the parliamentary elections, Barnier’s proposals to curtail the spending and balance the budget were met with resistance and resulted in “no confidence” vote. That leaves France unable to reform and seemingly stuck with a massive hole in the budget and increasingly lacking ideas how to fill it. As the French political drama continues, financial markets are voting with their feet by selling down French government debt and other related assets. Ironically, over a decade past the Greek financial crisis, the yields on the French government bonds have surpassed those of Greek government bonds, as investors apparently grew ever more concerned about the finances of France.

Yields on 10 year government bonds of Greece and France

Source: Investing.com

Confusion in the markets over South Korea’s martial law

On the other side of the world in South Korea, the political drama early December has spilled over into uncharted territory. President Yoon Suk Yeol has unexpectedly announced martial law in the country to deal with perceived threats from the neighboring North Korea. At least in theory it would mean that the previously functioning democratic system would be curtailed by accumulating power in the hands of a single person and increased army presence in the society. Trouble is, there was no perceived spike in North Korean threat at the time and the wide range of policymakers have lined up to disagree. The confusion has peaked as parliament members brawled their way through the soldiers to vote the martial law down in just a few hours’ time after it was imposed. While feared to be verging onto increasingly dangerous and unexpected path, South Korea has experienced some extremely shaky financial market’s reactions with equities’ Kospi index diving over 5% in a few days and the Korean Won dropping sharply in the currency market. Naturally, as South Korea constitutes a substantial portion of the Emerging Markets positioning in the investment portfolios, investors will be following the situation closely so as to assess the medium-term impact of this heightened confusion in the otherwise Asian success story.

ECB delivers another rate cut

In tune to the festive mood in mid-December, the European Central Bank has announced its decision to lower the interest rates for the fourth time, already, this year. The key ECB deposit rate was lowered by 0.25% to the new level of 3%, thus indicating further push by the central bank to stimulate the economy. While commenting on the decision during the press conference, ECB representatives have shared their intention to lower the rates further still towards a less restrictive level. As investors are pretty much accustomed by now to a regular lowering of interest rates by ECB, the attention of the market will shift on to eventual target level of interest rates. While the medium-term target level of interest rates is obviously unknown, many market participants forecast the key Euro zone interest rate will move closer to 1.75-2.5% range in time.

FED serves a hawk for Christmas

On the other side of the Atlantic, FED has seemingly delivered just as uneventful decision to lower the interest rates for the third time in a row to the new range of 4.25-4.5%. While the decision itself was widely expected, Federal Reserve has caught the markets by surprise in updating their plans for the next year. According to the updated forecast, the US central bank is going to reduce the rates twice next year by 0.25% each time. That is less than some market participants were expecting, as the many of them forecasted three quarter-point cuts in 2025. As the slightly changed FED stance signals there will be less monetary stimulus than expected, the markets have reacted substantially, with S&P 500 brushing off all the gains for the first half of the month in a single session by dropping nearly 3%, while US Dollar has gained versus other currencies to reflect the higher expected interest rates on the currency.

Market view

The investors’ optimism seems to sustain itself in the face of political challenges, while supported by the ongoing easing of interest rates by central banks, in general. With that said, any changes in the monetary policy can and will affect the markets substantially, with investment portfolios affected by the fluctuations in the asset prices as well as the currency movements. Going forward, financial market participants will keep a curious eye on the future profit developments of the leading market companies to assess the further direction for the financial markets. In addition, the extra scrutiny will be directed at the policy set by the central banks to assess the impact on the fixed income portion of the portfolios.

Warnings

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from the Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, represented within the Republic of Latvia by Luminor Bank AS Latvian branch, reg. No 40203154352, address: Skanstes iela 12, LV-1013, Riga, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Latvian Financial Supervisory Authority (Finanšu un kapitāla tirgus komisija). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Latvia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question, and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument, a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to internal rules on sound ethical conduct, management of inside information, handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.