Markets cooled on the sugar highs

- US debt gets downgraded

- Stocks recede on resilient economic data

- Real estate slowdown in the US

- Home improvement in the spotlight

The truly optimistic month of July was followed by the due correction in August – only to end the month on the optimistic tone, again. Pretty much all the global stock indexes have reached their low point in mid-August before recovering some of the lost ground by the end of the month. Investors could see the markets seesaw in the wake of stronger-than-expected US economic data, interest rates’ expectations and US credit downgrade among other developments. For the month of August, Developed markets’ stock index MSCI1 World has retreated -0.84%, while emerging markets stocks’ index MSCI Emerging Markets has dropped -4.67%. At the same time, US bond yields have risen slightly, too, with 10-year US Treasury bond yields rising to 4.10% (3.95% 1 month ago), while German 10-year Bund yields ended at 2.47% (in comparison to 2.49% a month ago).

Fitch downgrades US

The beginning of August was marked by quite an extraordinary event of Fitch Ratings downgrading US debt rating from the highest possible AAA one notch down to AA+ rating, thus – at least the theory goes - indicating slightly higher chance of default on the US sovereign debt. Fitch is one of the three main credit rating agencies (together with Moody’s and S&P) and is widely followed by the investment community. Until now, only S&P had its US debt rating rated at AA+, having downgraded it back in 2011 after a highly charged political drama over the debt ceiling. Interestingly, the move by Fitch this time comes in full two months after another similar debt-ceiling showdown in Washington. As it could be expected, the decision was met with criticism from the US government and a surprise from many market participants on the timing, as many of the reasons given for the downgrade could have well been applied pretty much any time during the recent years. Either way, no matter the short term upset from the US Treasury, this downgrade will most likely have no substantial effect on the US Treasuries’ pricing or the US debt capital markets, in general.

Interest rates scare the investors out of stocks

During the month of August the largest economy in the world – the US – has been showing signs of economic resilience in the face of steeply hiked interest rates over the recent months. Unemployment data, retail trade figures forced the market participants to reconsider their previous estimates on short-lived high interest rates, as it is becoming evident that higher-than-usual interest rates may need to be kept for longer than expected. This is naturally putting the brakes on the equity valuations, as higher-for-longer interest rates mean discounted future profits of companies are less valuable thanks to higher yielding alternatives (e.g. bonds). As the market participants have been digesting the possibility of higher interest rates for the foreseeable future, some of the high-flying segments of the stock market took a hit. Evidently, the technology sector – especially the highly volatile segment of the unprofitable technology companies. In many cases, low interest rates over the years had caused many investors to look for alternatives, even if the alternative happens to be a company with forecasted profits far away into the future. Now that the interest rates are so much higher than in previous years, these companies look increasingly vulnerable. As some investors are re-focusing back to more traditional yield-bearing securities, the technology-heavy Nasdaq composite index took a larger hit of -7.4% by mid-August, before recovering bigger share of the losses by the end of the month.

Housing activity slow in the US

On the back of rising interest rates across the globe and locally in the US, the 30-year mortgage rates in the US (mortgages in the US tend to have fixed rates across the mortgage lifespan) have topped 7% - the highest level American homebuyers had to pay on their mortgage loans since 2001. This is bound to have a substantial effect on the US real estate market, as only one third of housing transactions are executed on all-cash basis (i.e. the rest of the two thirds of transactions involve mortgage financing). 33,4% all-cash ratio itself in the US is sharply up since the early Covid-19 days in 2020 April, when low interest rates caused only ~20% of homebuyers to avoid a mortgage whatsoever.

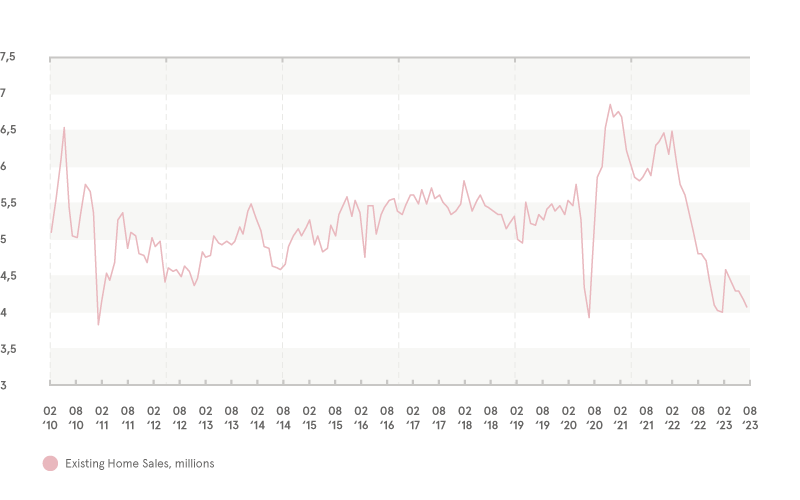

Coupling the high interest rates with the now-chronic shortage of housing supply in the US, the number of transactions, measured by Existing Home Sales in the US have fallen to the lowest level 2010, indicating a sharp slowdown in the US real estate market.

Existing Home Sales, millions

Source: Independent.com

Home improvement in the spotlight

This sort of background may not be the best for home-improvement leaders in the US - Home Depot and Lowe’s - which in spring have both lowered their profit expectations for 2023. The results for the 2023 Q2 have shown both of the companies experiencing slowdown in home improvement spending, thanks to housing market slowdown together with the inflationary worries by the consumers. However, the slowdown for now seems to be smaller-than-expected by the market participants and the companies’ representatives stay cautiously optimistic about the rest of the 2023 trading activity.

As the home-improvement sector is obviously a big ticket discretionary spending by the consumer, the surprises on the positive in this sector may bode well for the rest of the US economy, as this would indicate increasing consumer confidence and willingness to spend, hence the decreasing chances of severe recession ahead.

Market view

Luminor House ViewThere has been no major change in the market positioning by our investment team in August. We see the relative retreat in equities as a natural response to increased medium term competitiveness of the fixed income instruments. Should these circumstances be expected to continue, we would take appropriate steps to re-focus the investment portfolios to take advantage of the changed market realities.

Luminor House View

1 Morgan Stanley Capital International (MSCI) is an investment research company which, among other services, focuses on financial market indexes.

Warnings

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from the Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, represented within the Republic of Latvia by Luminor Bank AS Latvian branch, reg. No 40203154352, address: Skanstes iela 12, LV-1013, Riga, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Latvian Financial Supervisory Authority (Finanšu un kapitāla tirgus komisija). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Latvia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question, and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument, a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to internal rules on sound ethical conduct, management of inside information, handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.