Turning the page

- U.S. elections bring more clarity than expected

- Earnings season reflects resilience

- PMI’s showing mixed business activity in different regions

November brought much needed clarity to the markets, with a clear U.S. election outcome reducing uncertainty and driving a strong post-election rally. Corporate earnings showed resilience, with many companies delivering strong results, further boosting confidence in the economy. At the same time, global data revealed challenges, while the U.S. economy stood out for its strength. As markets head into a seasonally strong period, investors are focused on upcoming policy changes and economic trends to guide their next moves.

As a result, developed markets’ equities (measured by MSCI World index in EUR) have risen by 7.5%, while emerging markets’ equities (measured by MSCI Emerging Market index in EUR) have declined 0.9%. During the same period yields on bonds have declined, with 10-year U.S. Treasury bond yields decreasing to 4.18% from 4.28% a month ago, while German 10-year Treasury bond yields have decreased to 2.08% from 2.4% a month ago.

Election clarity restores market confidence

Election season brought its share of twists and surprises, but the outcomes are now largely settled. Donald Trump’s decisive win, along with Republican control of the Senate and the House of Representatives, defied predictions of a close or disputed race. Leading up to the election, market volatility increased, as is often the case during uncertain times. Now, with clarity restored, volatility has subsided, and the S&P 500 delivered one of the strongest-ever post-election rally, rising 2.5%. Although uncertainty remains over which campaign promises will translate into actionable policies, when they will be implemented, and their potential effects, the underlying market fundamentals remain broadly positive. As attention shifts to anticipated policy changes, these fundamentals are likely to continue guiding the market’s trajectory.

Earnings drive optimism

This earnings season has been marked by robust corporate performance, with results generally exceeding expectations in key sectors. NVIDIA (leading semiconductor and AI technology company) has taken center stage, as the world’s largest company by market capitalization delivered strong earnings and revenue growth fueled by increasing demand for AI-driven solutions. While sales and profits showed impressive year-over-year growth, the company’s forward guidance signaled a modest slowdown in momentum. Other corporate giants have also reported solid results, reflecting resilience in consumer spending and sustained demand. However, cautious management outlooks in some cases underscore ongoing uncertainties around economic conditions and future demand trends. Overall, the earnings season has reinforced confidence in the underlying strength of the economy, though markets remain attentive to signals of potential slowdowns in key growth drivers.

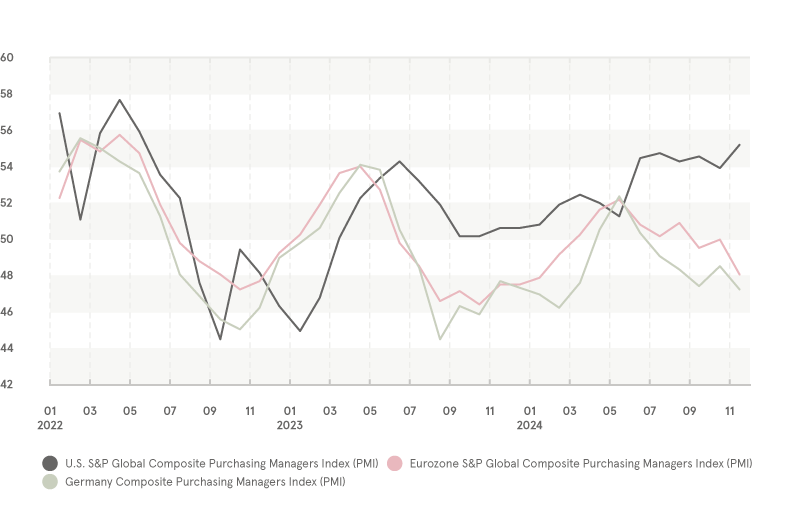

Mixed signals in global PMI trends

Recent data from the November S&P Global Purchasing Managers' Index (PMI) highlight ongoing economic challenges in global markets. The eurozone composite PMI dropped to 48.1, the lowest since January, signaling contraction (readings below 50 indicate shrinking activity). Germany, the region’s largest economy, has been a key driver of this slowdown, with its composite PMI falling to 47.3 and staying in contraction since June. Manufacturing weakness continues to weigh heavily, with both German and eurozone manufacturing PMIs contracting since mid-2022. In contrast, the U.S. economy stands out for its strength, as the composite PMI rose to 55.3 in November - a 31-month high, boosted by strong performance in the services sector. These contrasting trends highlight the relative resilience of the U.S. economy, which continues to outperform many international markets.

Global Composite PMI Trends: U.S., Eurozone, and Germany (Jan 2022 – Nov 2024)

Source: Investing.com

Market view

As the post-election landscape takes shape, markets are set to focus on long-term fundamentals, supported by solid economic conditions and earnings growth, led by the U.S. While gains may moderate after a strong rally since October 2022, November and December historically offer seasonally strong performance, particularly in election years. However, some gains from the post-election rally may already be priced in, and policy uncertainty could spark periodic volatility, but assuming no major shocks, pro-growth policies and a resilient economy should provide a stable foundation for the markets to navigate ahead. Investors will likely keep a close eye on economic data and policy developments to gauge the market's next direction.

Warnings

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from the Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, represented within the Republic of Latvia by Luminor Bank AS Latvian branch, reg. No 40203154352, address: Skanstes iela 12, LV-1013, Riga, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Latvian Financial Supervisory Authority (Finanšu un kapitāla tirgus komisija). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Latvia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question, and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument, a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to internal rules on sound ethical conduct, management of inside information, handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.